Piggyback & second lien financing are creative structures designed to reduce upfront cash, navigate loan limits, cut out PMI and support long-term financial strategy.

What Is Piggyback & Second Lien Financing?

Piggyback & second lien loans involve using a secondary loan alongside a primary mortgage to achieve a specific strategic goal — often to reduce upfront cash requirements, avoid certain loan limits, or preserve liquidity.

These structures are not one-size-fits-all.

They require careful planning, timing, and alignment with the borrower’s broader financial picture.

Common Use Cases

When These Structures May Make Sense

• Reducing the amount of cash needed at closing

• Avoiding jumbo loan thresholds

• Preserving liquid assets for reserves or investment

• Structuring around short-term or transitional needs

• Navigating property or underwriting constraints

Every scenario is evaluated on merit — not assumptions.

Why Strategy Matters Here

Piggyback and second lien loans can be powerful tools — or expensive mistakes — depending on how they’re structured.

Key considerations include:

• combined loan-to-value limits

• interest rate interaction between loans

• repayment alignment

• refinance and exit planning

• long-term cost vs. short-term benefit

I evaluate these structures not just for approval — but for sustainability.

What I Help Protect Clients From

This mirrors your investor page style and builds trust.

• Over-leveraging without a clear exit plan

• Short-term savings that create long-term stress

• Misaligned second liens that limit future refinancing

• Underestimated total borrowing costs

The goal is leverage with intention — not leverage for leverage’s sake.

Explore This Strategy

Clarity first. Structure second.

Piggyback Second & Second Lien Financing — FAQs

Not sure if this structure fits your situation? That’s exactly the conversation worth having.

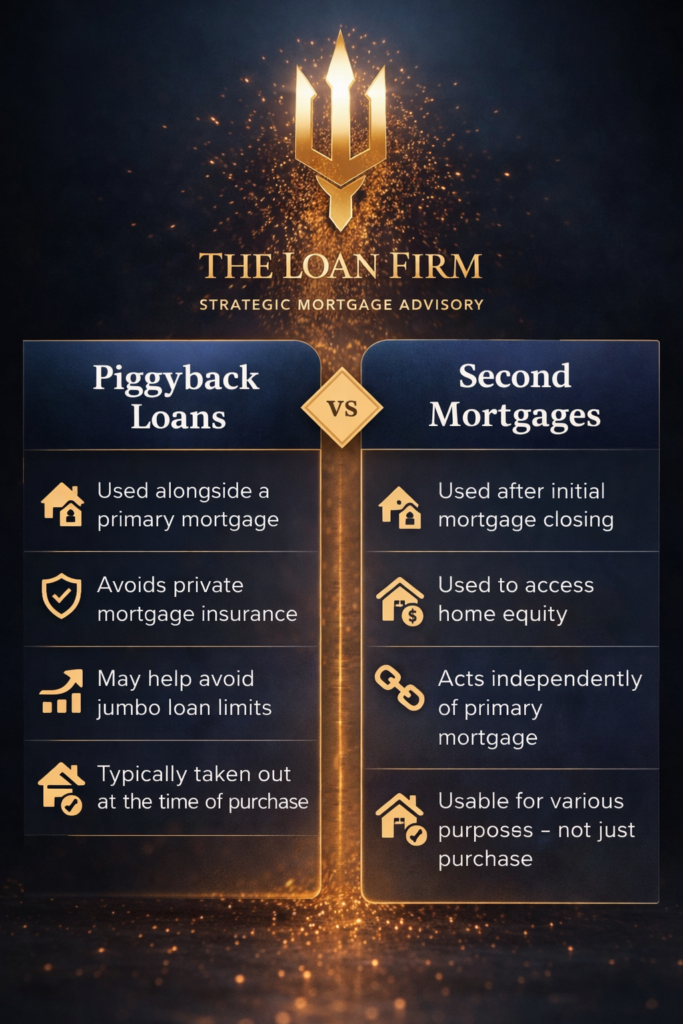

What is a piggyback loan?

A piggyback loan uses two mortgages simultaneously to finance a home purchase or refinance — typically a first mortgage paired with a second loan (often structured as 80/10/10 or 80/15/5)

Why would someone use a piggyback loan?

Common reasons include:

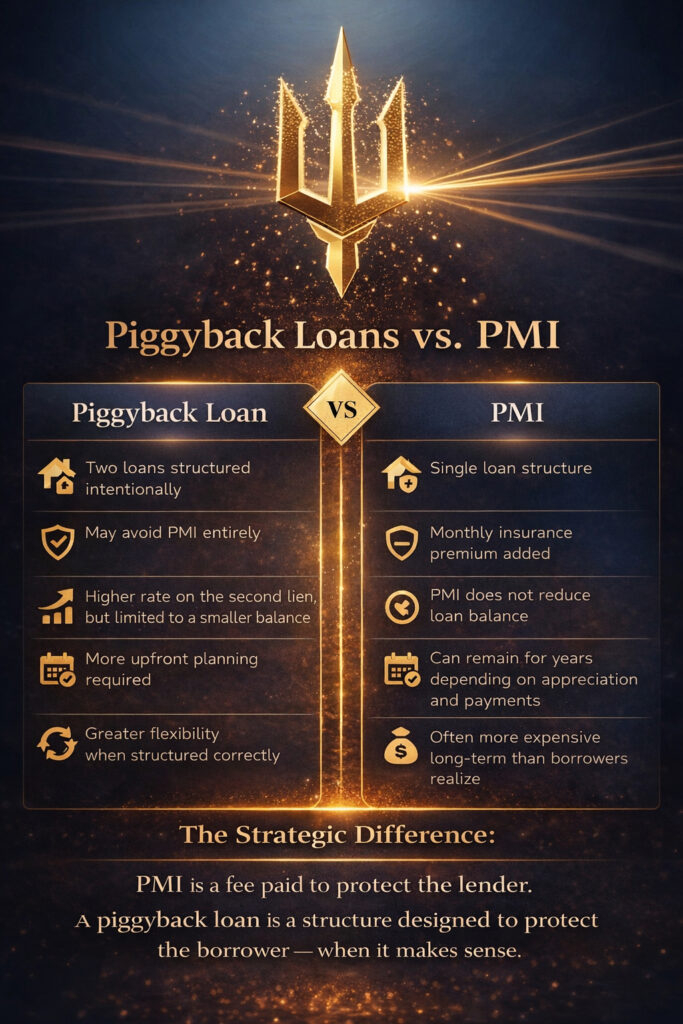

• Reducing or avoiding private mortgage insurance (PMI)

• Lowering the first mortgage loan amount

• Staying under conforming loan limits

• Reducing upfront cash requirements

Is a piggyback loan the same as a second mortgage?

Not exactly.

• Piggyback loan: Two loans originated at the same time

• Second mortgage / second lien: An additional loan added later, behind an existing first mortgage

Both are second-position liens, but the timing and purpose differ.

What is a second lien mortgage?

A second lien mortgage is a loan secured against a home in addition to an existing first mortgage. It may be used for:

• Debt consolidation

• Renovations

• Cash flow management

• Strategic leverage

Does a second mortgage replace my first mortgage?

No.

A second mortgage sits behind the first mortgage and does not change the terms of the original loan.

Are interest rates higher on second mortgages?

Yes — typically.

Second liens carry more risk for lenders, so rates are usually higher than first mortgages. Strategic structuring matters here.

Are monthly payments required?

Yes.

Unlike reverse mortgages, piggyback loans and second liens require monthly payments, including principal and interest.

Can piggyback loans help buyers avoid PMI?

Often, yes.

By keeping the first mortgage at or below 80% loan-to-value, PMI may be avoided — depending on loan structure and lender guidelines.

Are piggyback loans risky?

They can be — if structured incorrectly.

That’s why evaluating cash flow, future refinancing plans, and long-term affordability is critical.

Can I refinance later if I use a piggyback loan?

Yes, but coordination matters.

Refinancing may require:

• Subordination agreements

• Paying off or restructuring the second lien

• Careful timing

This is where planning ahead saves money and stress.

Do piggyback loans work for jumbo buyers?

Sometimes.

They can be used to stay below conforming loan limits or reduce jumbo exposure, but not all lenders allow this structure.

Can second liens be fixed or adjustable?

Yes.

Second mortgages may be fixed-rate or adjustable, depending on the program and borrower profile.

Do second mortgages affect credit and debt-to-income ratios?

Yes.

Both loans are included in qualifying calculations and must fit within responsible debt guidelines.

Is a HELOC the same as a second mortgage?

Not exactly.

• HELOC: Revolving line of credit with variable payments

• Second mortgage: Fixed loan with defined terms

Each serves different financial strategies.

Can piggyback loans be used for investment properties?

Sometimes — program dependent.

Owner-occupied homes typically have more flexible options.

Is this a good option for everyone?

No.

Piggyback and second lien financing should be used intentionally, with a clear exit strategy and long-term plan.

Why does structure matter so much with second liens?

Because mistakes here can:

• Complicate refinancing

• Increase long-term interest costs

• Limit future flexibility

The structure should support goals — not trap borrowers.

How does The Loan Firm approach piggyback and second lien loans?

As a strategy, not a shortcut.

Every structure is evaluated through:

• Cash flow

• Future flexibility

• Risk tolerance

• Long-term outcomes

Official & Consumer-Friendly Resources

🔱Consumer Financial Protection Bureau — Second Mortgage / Junior Lien

Defines second mortgage loans and junior liens, how they work, and what they mean for homeowners. CFPB: What is a second mortgage loan or junior-lien?

🔱Consumer Financial Protection Bureau — Piggyback Second Mortgage

Explains what a piggyback second mortgage is, how it’s structured, and how it was historically used to avoid PMI. CFPB: What is a piggyback second mortgage?